The market’s bullish trend remained strong, extending the rally into its second week. The sharp rise in the index was driven by broad gains across sectors after the RBI cut cash reserve ratio by 0.5% to 4% to improve liquidity. The NIFTY50 index rose over 2% to end the week at 24,677.

Apart from FMCG (-0.3%), all other major sector indices ended the week in the green, with real estate (+5.2%), PSU banks (+5.0%) and consumer durables (+5.0%) leading the way. It has risen. .

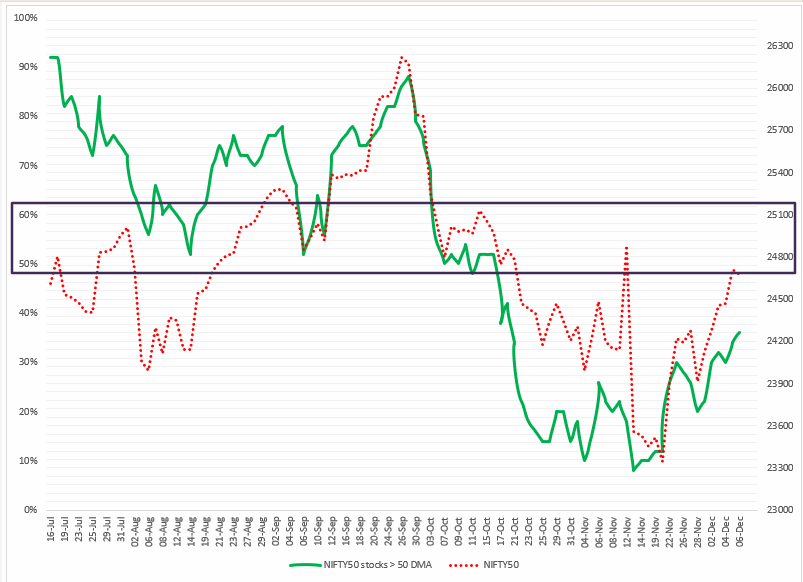

index width

The NIFTY50 index remains positive with more than 30% of its constituents trading above their respective 50-day moving averages (DMAs). However, the broader index width remains below the important 50% threshold, as shown in the chart below. If the index regains 2 of the 5,000 zone on a closing price basis and the reading of the breadth indicator is above 50%, the trend could definitively shift to the bullish direction. Until these conditions are met, the trend is likely to remain flat to slightly bullish.

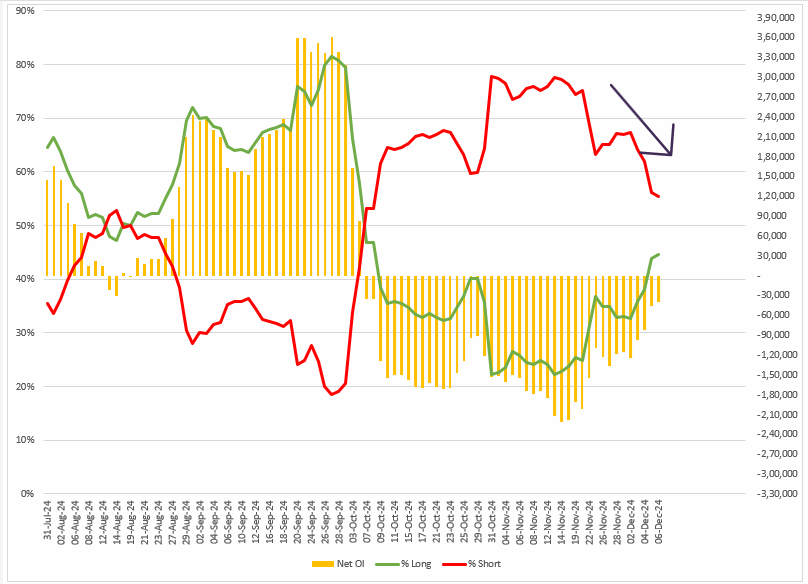

FII position in the index

Foreign institutional investors (FIIs) reduced net open interest (OI) in index futures by 68% last week, to a net OI of 39,000. FII began the December series with a long-to-short ratio of 33:67, but as of December 6, this ratio stands at 45:55, indicating a significant unwinding of net short contracts .

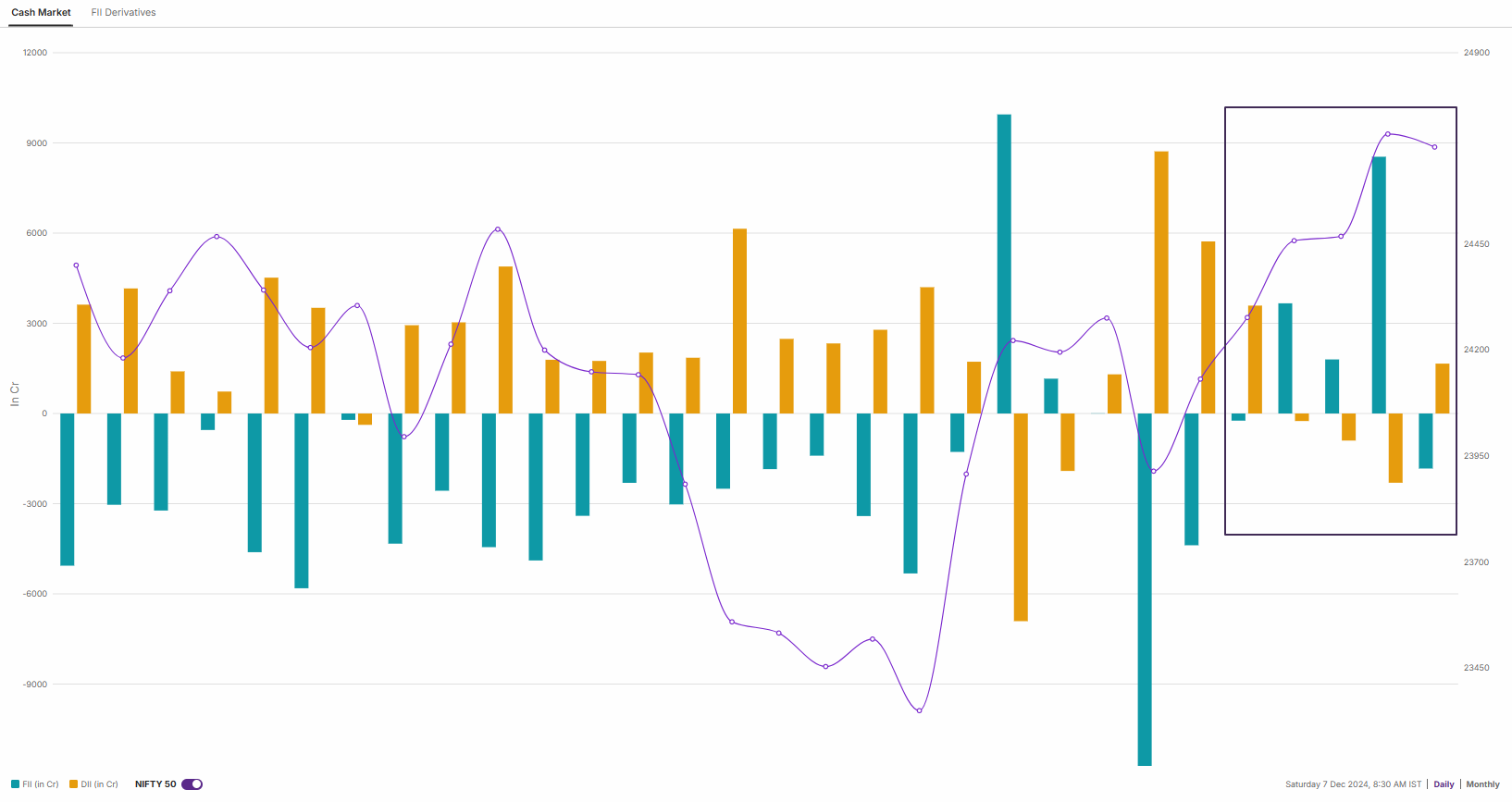

The reduction in net empty open interest in FII index futures was done in line with the spot market. FIIs turned buyers in the first week of December, buying shares worth Rs 11,933 crore. Meanwhile, domestic institutional investors (DIIs) maintained their buying momentum, purchasing shares worth Rs 1,792 crore, taking the net institutional investor activity to Rs 13,726 crore.

Outlook for NIFTY50

After confirming a hammer candlestick pattern in the week ending November 22, the NIFTY50 index extended its gains for the third consecutive week. The index regained its 20-week exponential moving average (EMA) and closed above last week’s high, indicating bulls continued to be in control throughout the week. However, the sharp volatility widened the index’s trading range to 3.5%, which was above the index’s average range.

Next week, traders can monitor the previous week’s high and low prices. Unless the index closes above these levels, the trend is likely to remain sideways. Breaking above and below these levels on a closing price basis on the daily chart could provide further directional clues.

SENSEX outlook

SENSEX also extended its bullish momentum for the third week in a row, regaining its 20-week EMA on a closing price basis. However, the index witnessed resistance near the 82,300 highlight zone and is facing rejection from higher levels, indicating the presence of sellers around these levels.

Looking ahead to next week, the index is likely to consolidate gains within last week’s range, with immediate support near 79,300 and resistance near 82,300. Unless the index breaks out of this range on a closing price basis, the trend is likely to remain within the range.

🗓️Key events to watch: Globally, investors will be keeping an eye on the November Consumer Price Index (CPI) report, scheduled for release on December 11th. Market participants expect annual inflation to rise slightly to 2.7% year-on-year in November. Meanwhile, core CPI, which excludes volatile food and energy prices, is expected to stabilize at 3.3%.

Domestically, the November inflation report is scheduled to be released on December 12th. According to market estimates, retail inflation could rise to 5.7% year-on-year, down from 6.2% in October.

📌Spotlight: All eyes were on banking and real estate stocks last week after the Reserve Bank of India (RBI) announced a 50 basis point cut in cash reserve ratio (CRR) on December 6th. CRR reduction provides banks with additional lending funds. , could stimulate credit growth and support economic activity.

Experts believe that lower CRR will improve liquidity in the system and have a positive impact on banks. However, it is important to note that the RBI has decided to keep the repo rate at 6.5% for the 11th consecutive time since February 2023. This highlights the RBI’s cautious stance amid persistent inflationary pressures and slowing growth. The central bank also raised its inflation forecast for fiscal 2025 to 4.8% from 4.5%.

🛢️Oil: Oil prices fell more than 1% last week as sentiment turned bearish amid expectations of oversupply in 2024 due to weak demand. This came despite OPEC+ delaying production increases and extending deep production cuts until 2026.

OPEC+, which accounts for about half of the world’s crude oil production, announced that it would postpone its planned production increase by three months until April 2024. However, sluggish global demand, particularly from China, the largest importer, and rising supply from the United States continue to weigh on it. price. Against this backdrop, Brent crude oil fell 1.4% on the week to settle at $71 per barrel, while US West Texas Intermediate (WTI) fell 1.5% to $67 per barrel. Finished the week.

📊Stocks to watch: Based on price and open interest, we saw secular gains in Jubilant Foodworks, Metropolis, PB Fintech (Policy Bazaar), and Escorts Kubota. Similarly, to track OI and price losers, log into Upstox ➡️F&O➡️Futures Smart List ➡️OI Losers.

📓✏️ Bottom line: In last week’s blog, we predicted that the NIFTY50 index would remain in the 24,600-23,300 range with a breakout likely to be a further directional clue. During a volatile session that coincided with the weekly options expiration, the index broke through a resistance zone, indicating near-term bullish momentum.

Meanwhile, sharp swings in both directions and increased volatility pushed the index’s trading range to more than 3.5%, above average. Nevertheless, the index ended above last week’s high, reflecting buying interest at low levels.

In the coming week, traders should focus on the previous week’s highs and lows as key levels. The trend is likely to remain range bound unless the index closes above these levels on the daily chart.

For updates on intraday ranges and corrections to these levels, check out our daily morning trade setup blog, published at 8 a.m. before the market opens.

Disclaimer:

Derivatives trading should only be undertaken by traders who fully understand the risks involved and strictly apply risk mechanisms such as stop losses. This information is solely for Client’s consumption and such material may not be redistributed. We do not recommend any particular stocks, securities or trading strategies. Securities referenced are illustrative only and are not recommendations. Stock names mentioned in this article are used solely to illustrate the analysis methodology. Please use your own judgment before investing.